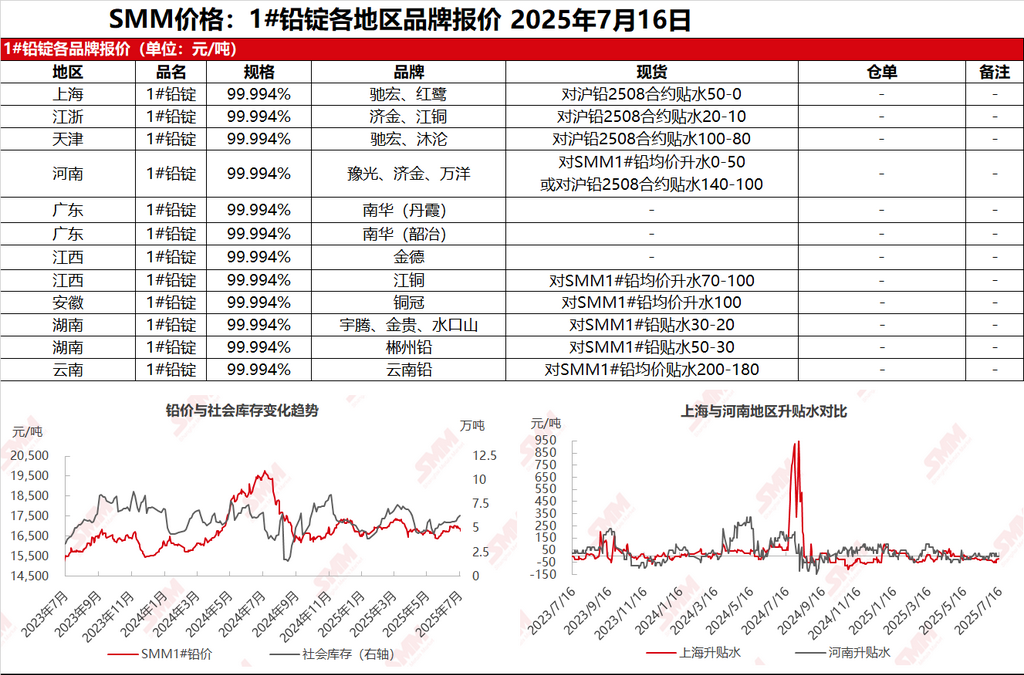

SMM News on July 16: In the Shanghai market, Chihong and Honglu lead were quoted at 16,845-16,905 yuan/mt, with discounts of 50-0 yuan/mt against the SHFE lead 2508 contract. In the Jiangsu-Zhejiang market, Jijin and JCC lead were quoted at 16,875-16,895 yuan/mt, with discounts of 20-10 yuan/mt against the SHFE lead 2508 contract. The center of SHFE lead prices moved further downward, and some suppliers narrowed their discounts, but downstream enterprises maintained a strong wait-and-see sentiment, with limited inquiries and sluggish spot order market transactions. Additionally, there were still differences in the supply of primary lead smelters between the north and the south, and the premiums and discounts of quotations also expanded simultaneously. Premium quotations gradually emerged in the north (against the SMM #1 lead average price), while discounts expanded in the south. Moreover, the reluctance to sell at low prices among secondary lead smelters increased, with some smelters suspending quotations, while others leaned towards premium quotations. Secondary refined lead was quoted at discounts of 50 yuan/mt to premiums of 50 yuan/mt against the SMM #1 lead average price ex-factory.

Other markets: Today, the SMM #1 lead price fell by 100 yuan/mt compared to the previous trading day. In Henan, smelters had low inventory, and some enterprises suspended spot order shipments. Suppliers further narrowed their discounts, quoting at discounts of 140-100 yuan/mt against the SHFE lead 2508 contract ex-factory. In Hunan, suppliers quoted at discounts of 30-20 yuan/mt against the SMM #1 lead average price ex-factory, and small smelters quoted at discounts of 50-30 yuan/mt. However, downstream enterprises had low enthusiasm for purchases, resulting in sluggish market transactions. In Jiangxi, suppliers quoted at premiums of 70-100 yuan/mt against the SMM #1 lead ex-factory. Lead consumption remained weak, and coupled with the expected increase in social inventory of lead ingots around the delivery of the SHFE lead 2507 contract, downstream enterprises were generally cautious about purchasing amid fears of price declines. After the continuous weakening of lead prices, there was a coexistence of low prices from smelters and downstream risk-aversion and wait-and-see sentiment. Only some traders were interested in purchasing at low prices, and overall market transactions remained sluggish.